2-1 Buy Down

6.5% = 4.5%

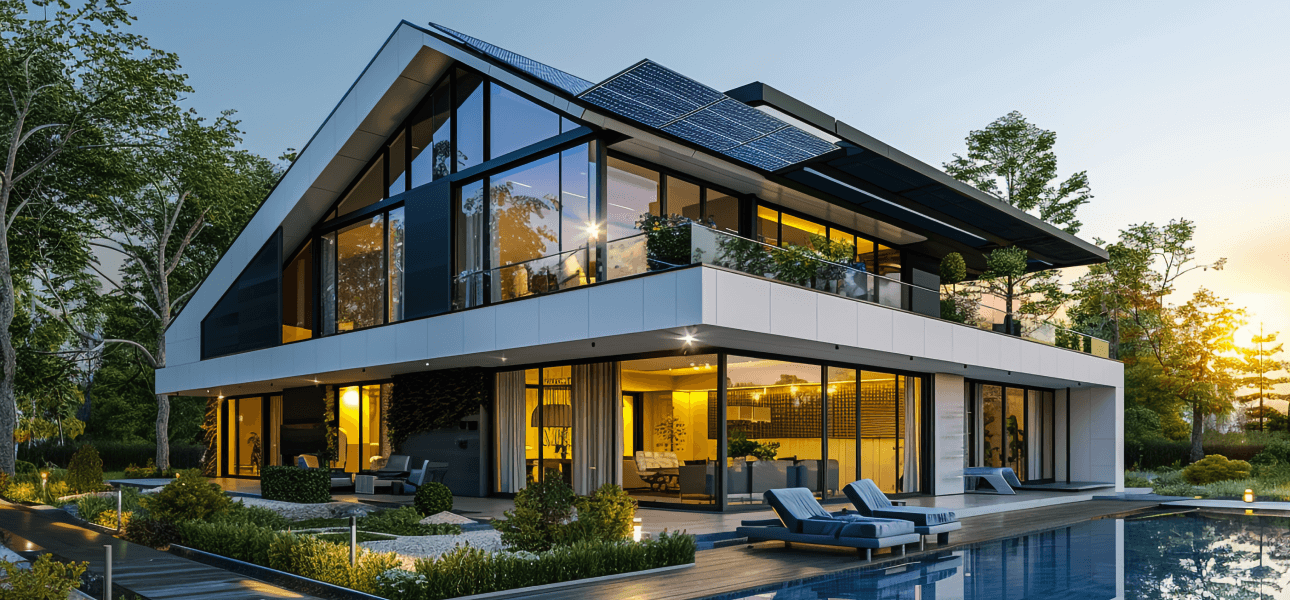

Las Vegas Market

A 2-1 buydown is a temporary mortgage rate reduction strategy that helps make homeownership more affordable during the first two years of a loan. It allows buyers to ease into their full mortgage payment while adjusting to new housing expenses. With a 2-1 buydown, the interest rate is reduced by 2% in the first year and 1% in the second year. By the third year, the loan adjusts to the full note rate for the remainder of the term. For example, if the permanent interest rate is 6%, the buyer would pay 4% in year one, 5% in year two, and 6% from year three onward.

The cost of the buydown is typically paid upfront in a lump sum and is often funded by the seller as a concession, though buyers or builders can also pay for it. The funds are placed in an escrow account and used to subsidize the reduced payments during the first two years. Unlike an adjustable-rate mortgage, the note rate itself does not change—only the payment is temporarily reduced. A 2-1 buydown can be used with conventional loans backed by Fannie Mae or Freddie Mac, as well as loans insured by the Federal Housing Administration and guaranteed by the U.S. Department of Veterans Affairs, provided guidelines are met.

For buyers, the primary benefit is improved short-term affordability. It can help households who expect future income growth or who want payment relief while settling into a new home. It may also increase purchasing power without permanently increasing the loan balance. However, buyers must qualify at the full note rate, not the reduced rate. It’s important to ensure the long-term payment fits comfortably within the budget. When structured properly, a 2-1 buydown can be a smart tool to create flexibility and reduce financial strain during the early years of homeownership.

Financing & Down Payment Assistance 702-673-8702

Air Condition

Heated Water

Hospital

Swimming Pool

High Speed WIFI

Click Here 2-1 Buy Down